WTF Dailies September 29, 2025

US stock futures climbed overnight Sunday as investors regrouped from a losing week that saw cracks emerge in AI-focused stock trading as well as surprise tariff announcements from President Trump for Oct. 1.

- US stock futures climbed overnight Sunday as investors regrouped from a losing week that saw cracks emerge in AI-focused stock trading as well as surprise tariff announcements from President Trump for Oct. 1.

- Meanwhile, a government shutdown remains possible by Wednesday this week, leaving an air of doubt over whether the government will release key economic data — including the highly anticipated jobs report on Friday. A meeting between Trump and congressional leaders is set for Monday, serving as potentially the last hope to avoid a shutdown.

- Most Asian stocks rose on Monday as technology shares rebounded from steep losses logged last week, although investors remained cautious before central bank meetings in Australia and India this week.

- Japanese shares lagged as strength in the yen pressured export-oriented stocks, while Indian markets nursed outsized losses from last week.

- Regional markets tracked some strength in Wall Street from Friday, where in-line inflation data helped traders maintain expectations for more interest rate cuts by the Federal Reserve. But sentiment towards U.S. markets was dented by fears of a looming government shutdown, which could occur later this week, while a flurry of more tariff announcements also weighed.

- Australia’s ASX 200 index rose 0.8% with focus chiefly on the conclusion of a two-day Reserve Bank of Australia meeting on Tuesday. Banks and gold stocks were the main boosts to the index.

- The RBA is widely expected to keep interest rates unchanged amid recent signs of inflation turning sticky, but could offer up some signals on a potential cut in November.

- “A 25bp cut is more likely in November, taking the policy rate to 3.35% for an extended period,” ANZ analysts said in a recent note, adding that Governor Michele Bullock was widely expected to reiterate the central bank’s data-driven stance on further easing, after about 75 bps of cuts so far in 2025.

- Recent data showing an unexpected increase in Australian inflation had dampened bets on more rate hikes by the RBA, which has maintained its stance of curbing inflation as a key goal.

- South Korea’s KOSPI and Hong Kong’s Hang Seng index were the top performers in Asia, rallying 1.1% and 1.5%, respectively.

- Regional tech shares rebounded after logging steep losses last week on some doubts over the artificial intelligence trade. Reports that the U.S. was mulling even more measures against imported semiconductors also rattled the sector.

- Tech was aided by a drop in Treasury yields, especially as U.S. PCE price index data on Friday read in line with expectations. The print drummed up bets on more interest rate cuts from the Fed, supporting Wall Street and also supporting risk into Monday’s Asian session.

- Broader Asian markets also mostly advanced. China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes rose 0.6% and 0.1%, respectively.

- Singapore’s Straits Times index rose 0.2%.

- Japan’s Nikkei 225 and TOPIX indexes slid 1.5% and 0.7%, respectively, as strength in the yen pressured export stocks. The yen was supported in part by a weaker dollar as markets bet on more U.S. rate cuts, while speculation over a rate hike by the Bank of Japan also helped.

- India’s Nifty 50 index rose 0.5% in early trade, rebounding from bruising losses last week. Indian markets have largely lagged their peers on concerns over more trade friction between Washington and New Delhi.

- The Reserve Bank of India is set to meet later this week, and is expected to leave its benchmark rate unchanged while slightly trimming its cash reserve ratio, representing some monetary easing.

- The RBI may face increased pressure to ease monetary policy further, as the Indian economy grapples with a 50% U.S. import tariff. New Delhi had doled out a series of tax cuts earlier in September to offset the economic headwinds from U.S. trade tariffs.

Market Close

- Equity markets closed higher on Monday, with mid-cap stocks leading large- and small-cap stocks. Sector performance was broadly higher, as consumer discretionary and technology stocks posted the largest gains, while energy and communication stocks trailed.

- Bond yields fell, with the 10-year U.S. Treasury yield at 4.14%, still above its recent low of 4.0% earlier this month.

- In international markets, Asia finished mostly lower overnight, while Europe was about flat. The U.S. dollar declined against major international currencies. In commodity markets, WTI oil traded lower on expected OPEC+ production hikes.

- Key economic releases scheduled for this week should provide updates on the labor market, though some data could be delayed in the event of a government shutdown. Job openings for August — to be released on Tuesday — are expected to dip to 7.1 million, from 7.2 million the prior month. Total nonfarm payrolls will provide a deeper look at the labor market on Friday, with forecasts calling for 50,000 jobs created in September, up from just 22,000 in August.

- The unemployment rate is expected to hold steady at 4.3%, while estimates are pointing to 3.7% hourly wage growth year-over-year, also in line with the August figure. With unemployment still relatively low and job openings modestly below the 7.4 million people who are unemployed, the labor market appears to be cooling but not collapsing, in our view. Despite the softer labor market, wage growth continues to outpace CPI inflation of about 2.9%, providing rising discretionary income to support consumption.

- With the current fiscal year ending on September 30 and no funding agreement in place, a government shutdown could begin on October 1. The U.S. House of Representatives recently passed a short-term funding measure, but the legislation faced resistance in the Senate as Democrats seek to reverse some of the health care cuts that were in the tax bill passed over the summer. If no agreement is reached, nonessential parts of the federal government would shut down, furloughing workers and halting some services until funding is restored.

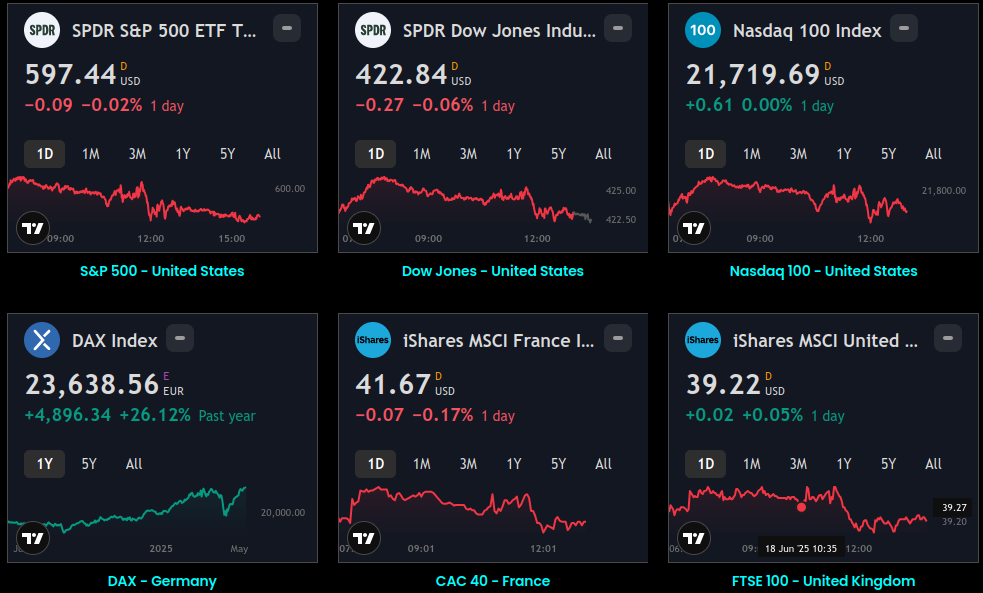

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.