WTF Dailies September 22, 2025

US stock futures edged lower Sunday evening as traders caught their breath following a milestone week that saw the Dow Jones Industrial Average and S&P 500 notch fresh all-time highs.

- US stock futures edged lower Sunday evening as traders caught their breath following a milestone week that saw the Dow Jones Industrial Average and S&P 500 notch fresh all-time highs.

- The rally followed the Federal Reserve’s quarter-point rate cut in its first since December. The move, widely expected, initially rattled markets but ultimately reassured investors that policymakers are leaning dovish as labor market signals weaken.

- This week, investors will get a fresh read on the Fed’s preferred inflation gauge, the personal consumption expenditures (PCE) price index. Economists expect the report to reflect sticky pricing pressures, though still tame enough to keep the central bank on its current policy track.

- Asian stocks were a mixed bag on Monday, with Japanese shares rebounding from prior losses despite a hawkish Bank of Japan, while Indian technology stocks slid on U.S. President Donald Trump’s crackdown against a major work visa category.

- Chinese stocks lagged, while profit-taking in major internet stocks and losses in BYD weighed on Hong Kong shares.

- Regional markets took some positive cues from record-high closes on Wall Street last week, as investors cheered an interest rate cut by the Federal Reserve. But this rally was seen cooling on Monday, with S&P 500 Futures down 0.1% in Asian trade.

- Focus this week is on a host of key economic indicators and Fed speakers, with Chair Jerome Powell set to speak on Tuesday.

- India’s Nifty 50 index opened mildly negative on Monday, pressured chiefly by losses in major tech and outsourcing stocks.

- The sector was rattled by Trump on Friday imposing a $100,000 annual fee on companies for issuing new H-1B worker visas.

- The visa has long served as a means for Indian tech companies to rotate their skilled talent into U.S. projects. The sector is also highly dependent on the U.S. for revenue, earning nearly 60% from overseas projects.

- Indian tech has benefited greatly from the outsourcing of U.S.-based labor and operations to cheaper, local businesses. Trump’s increased scrutiny of this practice could herald more headwinds in the coming months.

- Trump had last month also doubled tariffs against India to 50% over its buying of Russian oil.

- But bigger losses in Indian markets were stemmed by positive comments from Prime Minister Narendra Modi on Sunday. Modi said a recent round of consumer tax cuts enacted by his administration will boost economic growth.

- The Nikkei 225 and TOPIX indexes rose 1.5% and 0.9%, respectively, after falling from record highs on Friday.

- Losses in Japanese markets were spurred chiefly by the Bank of Japan, which kept interest rates unchanged on Friday, but signaled plans to begin offloading its massive holdings of exchange-traded funds.

- The BOJ’s move represents some more monetary tightening, and also heralds selling pressure on stocks most exposed to its ETF holdings, which come largely from the tech and chipmaking sectors.

- Still, losses in Japanese markets were stemmed by the BOJ’s planned annual sales representing only a small portion of its overall ETF holdings. BOJ Governor Kazuo Ueda also struck a largely moderate tone on Friday, and did not commit to any potential interest rate hikes.

- South Korean stocks also outperformed most of their Asian peers on Monday, with the KOSPI adding 0.9%.

- Samsung Electronics Co Ltd (KS:005930) was a major boost to the index, rallying as much as 5% after a host of reports said the company had earned NVIDIA Corporation’s (NASDAQ:NVDA) approval to supply advanced memory chips to the artificial intelligence major.

- The approval puts Samsung back in competition with rivals such as SK Hynix Inc (KS:000660) and Micron Technology Inc (NASDAQ:MU) in supplying advanced AI memory chips, which have proven to be an increasingly lucrative sector over the past two years.

- Broader Asian markets were a mixed bag. Hong Kong’s Hang Seng index fell for a third straight session from a four-year high, amid sustained profit-taking in local tech names.

- BYD (HK:1211) was a major weight on the Hang Seng, losing over 3% on a report that Warren Buffett’s Berkshire Hathaway (NYSE:BRKa) had entirely exited its position in the electric vehicle maker.

- China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes were flat, showing little reaction to the People’s Bank of China leaving its benchmark loan prime rate unchanged as expected.

- Focus is squarely on ongoing trade dialogue between the U.S. and China, with the two reaching consensus on the U.S. operations of TikTok last week.

- Australia’s ASX 200 rose 0.4%, while Singapore’s Straits Times index was flat.

Markets Close

- U.S. equity markets rallied at the start of the week, led by a surge in NVIDIA after its pledge to invest as much as $100 billion in Open AI. This helped push NVIDIA's stock price 4% higher, powering a 0.7% rise in the technology-focused Nasdaq index to new record highs. The positive tone was felt more broadly across the major U.S. indexes, with the S&P 500, Dow Jones Industrial Average and small-cap Russell 2000 all moving higher over the day.

- Gold also continues to rally, with prices hitting a new record above $3,700 per ounce, helped by a rise in ETF inflows into this asset class to a three-year high. Elsewhere, following a quiet start to the session, saw a modest sell-off in U.S. government bond markets, with the yields on Treasuries continuing to drift higher after the Federal Reserve Bank meeting last week.

- The dollar was a shade weaker against a trade-weighted basket of currencies, and WTI oil prices were down but remain in their recent $60-$65 per-barrel range.

- Late last week President Trump signed a proclamation that imposes a $100,000 fee for H1-B visas, with the administration clarifying over the weekend that this would apply to the application process for this work authorization. The H1-B visa program allows 65,000 work visas for high skilled degree holders annually, with a further 20,000 visas available for master's degree holders too. These visas are used heavily by technology companies, with computer-related occupations accounting for around 65% of approvals in 2023. It remains to be seen if the increase in the fee from $1,000 will be successfully challenged in the courts, but the move adds to the push from the administration to substantially tighten U.S. immigration policy. The effect of this adjustment is already showing up in aggregate labor-market statistics, with job gains in sectors reliant on immigration having slowed to a standstill this year.

- The Fed restarted its easing cycle last week but stopped short of promising that further cuts are on the way. Instead, it will likely be up to the data to determine the central bank's next steps, with this week's August personal consumption expenditures (PCE) report in focus. Economists can use consumer price index (CPI) and producer price index (PPI) data already released for August to quite accurately forecast this report, and are currently anticipating a reading of 0.3% month-over-month for headline PCE and 0.2% for the core reading.

- Economists are forecasting an acceleration in price pressures through the end of this year, as firms increasingly look to pass through the cost of higher tariffs to their end customers. This need not stop the Fed from easing, given that it expects these increases will be one-off inflation shocks. However, it might challenge market expectations that the central bank will cut interest rates by 25 basis points (0.25%) at both its October and November meetings.

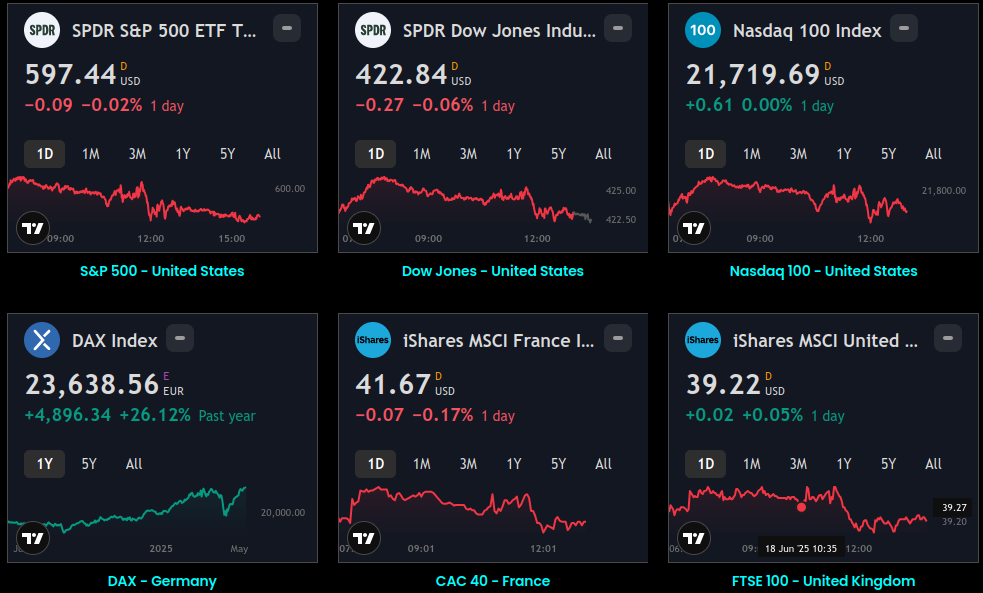

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.