WTF Dailies September 17, 2025

US stock futures crept down as traders awaited the conclusion of the Federal Reserve's two-day policy meeting, which is widely expected to to feature the first interest rate cut of 2025.

- US stock futures crept down as traders awaited the conclusion of the Federal Reserve's two-day policy meeting, which is widely expected to to feature the first interest rate cut of 2025.

- While a rate cut is seen as practically a done deal, the trajectory of interest rates going forward is less certain. Consequently, investors will also be watching for the release of the Fed's "dot-plot," which will offer insight into how many cuts the central bank anticipates for the rest of 2025.

- Wall Street will also be eager to hear Fed Chair Jerome Powell's remarks at a press conference following the decision, which begins at 2:30 p.m. ET.

- The Fed's next move comes amid growing concerns over the central bank's independence. While President Trump has lambasted Powell, he has also started to exert more direct influence over the Fed's ranks.

- The Senate confirmed Trump's nominee to the Federal Reserve Board in a tight vote on Monday evening, allowing Stephen Miran to vote this week. Before being confirmed, Miran said that he will not resign from his role as a White House advisor during his time at the Fed and instead will take a leave of absence so that he can return to the job later.

- At the same time, an appeals court on Monday rejected Trump's attempt to oust Fed governor Lisa Cook over alleged mortgage fraud. Cook thus remains on the board and will partake in policy decisions as court proceedings unfold.

- Asian shares were mixed on Wednesday as investors stayed cautious ahead of the U.S. Federal Reserve’s policy decision later in the day, while Japanese stocks hovered near record highs after trade data showed the country’s deficit shrank less than expected.

- Regional markets also tracked the subdued close on Wall Street overnight. Benchmark indices closed marginally lower on Tuesday, while futures tied to them traded largely unchanged in early Asia hours on Wednesday.

- Lower U.S. rates tend to support capital flows into Asia and ease pressure on regional currencies.

- Hong Kong’s Hang Seng index jumped 1.5% on Wednesday, remaining buoyed by tech sector gains.

- Investors welcomed Hong Kong Chief Executive John Lee Ka-chiu’s policy address on Wednesday, focusing on economic revitalization and enhancing residents’ quality of life.

- He reaffirmed the city’s 2025 growth forecast of 2% to 3% and emphasized the government’s commitment to improving housing, increasing workers’ wages, enhancing elderly care, and providing better prospects for youth.

- China’s blue-chip Shanghai Shenzhen CSI 300 rose 0.6%, while the Shanghai Composite index gained 0.4%, remaining near decade high levels.

- South Korea’s KOSPI slipped 0.7% on Wednesday, retreating after six straight sessions of record highs.

- Elsewhere, Australia’s S&P/ASX 200 fell 0.7%, while Singapore’s Straits Times Index edged 0.2% lower.

- India’s Nifty 50 traded 0.3% higher at market open.

- In Tokyo, the Nikkei 225 was largely unchanged, holding just below record highs of 45,055.0 points reached on Tuesday.

- The broader TOPIX index fell 0.6%.

- Trade data for August showed resilience despite tariff headwinds. Exports slipped 0.1% from a year earlier, less than forecasts for a 1.2% drop, while imports fell 5.2%.

- That left a trade deficit of 242.5 billion yen ($1.64 billion), narrower than the 325 billion yen shortfall expected by economists.

- Exports improved after the U.S. and Japan finalized a trade deal in August, capping U.S. tariffs on Japanese goods at 15%. Still, domestic demand in Japan remained weak, weighed down by high import costs and persistent inflation.

Market Close

- Equity markets finished modestly lower on Wednesday following the Fed's decision to cut the fed funds rate by 25 basis points (0.25%), as expected. Interest-rate-sensitive small-cap stocks led large- and mid-cap stocks. Financial and consumer staples stocks posted the largest gains, while the technology and industrial sectors trailed.

- Bond yields rose, with the 10-year U.S. Treasury yield at 4.07%. In international markets, Europe was mixed, led by the technology sector, as major U.S. technology companies announced investments in the U.K. during President Trump's visit to the country.

- The U.S. dollar strengthened against major international currencies. In commodity markets, WTI oil traded lower following gains in recent days that were driven by supply concerns following Ukrainian drone strikes on Russian oil infrastructure.

- The Fed's Open Market Committee (FOMC) cut its target range for the fed funds rate to 4.0% – 4.25% this afternoon, as widely expected. The Fed also updated its quarterly economic projections, in which the fed funds forecast – known as the "dot plot" – opened the door to an additional rate cut this year compared with the June release. The dot plot confirmed expectations for one rate cut next year, which would bring fed funds down to the 3.25% - 3.50% range. Bond markets are pricing in a faster pace of easing, with fed funds falling below 3% over the same timeframe, though the gap has narrowed. The Fed's new projection also reflected expectations for slightly faster economic growth, lower unemployment, and higher inflation, compared with the figures released in June. Overall, the Fed's decision and projections appear to have largely met expectations, resulting in a muted reaction in stock and bond markets.

- Bond yields rose modestly, with the 10-year Treasury yield at 4.07%. The recent trend has been lower, in which the benchmark Treasury yield briefly matched its lows for the year reached in April. Lower yields have driven solid fixed-income performance. As the Fed likely cuts rates in the months ahead, short-term Treasury yields — particularly those on T-bills — should drop along with the fed funds rate.

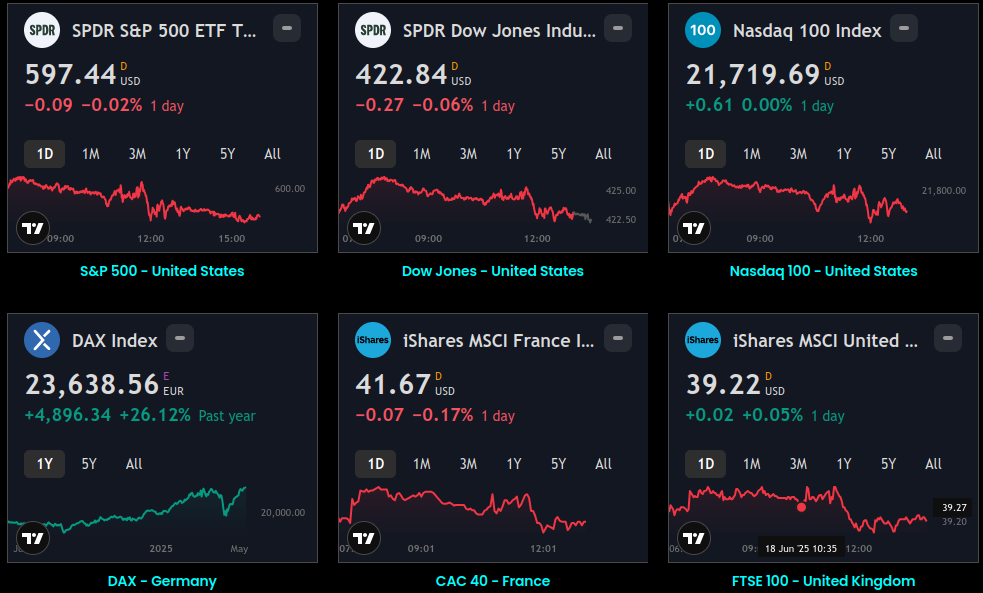

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.