WTF Dailies September 11, 2025

US stock futures inched up as Wall Street's attention turned from an upbeat day marked by renewed AI fervor to the next tranche of critical economic data.

- US stock futures inched up as Wall Street's attention turned from an upbeat day marked by renewed AI fervor to the next tranche of critical economic data.

- The final data point on inflation that is set to land before the Fed's September 19th meeting arrives Thursday. August's Consumer Price Index (CPI), due at 8:30 a.m. ET, is expected to show inflation remained sticky last month, with headline prices rising. Investors will be vigilant for indications President Trump's tariffs are impacting prices.

- The CPI reading, however, is not expected to pack enough punch to dissuade the Fed from cutting rates in light of a significant slowdown in the labor market. Markets are pricing in a 92% chance of a 25 basis point cut at the Fed's meeting, according to the CME FedWatch tool, and an 8% chance of a larger half-point reduction.

- The US Department of Labor's Thursday release of weekly jobless claims will consequently be of more interest than usual to Wall Street.

- Most Asian stock markets rose on Thursday, with China leading gains on renewed U.S. artificial intelligence optimism, while Japan’s Nikkei notched fresh record highs amid political turmoil at home.

- Traders kept a close eye on U.S. consumer price inflation data due later in the session.

- Japan’s Nikkei 225 index jumped over 1% on Thursday to hit a fresh record high of 44,288.47 points, reaching peaks above 44,000 points for the second time this week.

- The move comes after Japanese Prime Minister Shigeru Ishiba stepped down on Sunday following heavy election losses and growing internal party dissent.

- This sparked expectations that his successor may pursue more expansionary fiscal and monetary policies.

- Market sentiment was also supported this week by confirmation of a U.S.-Japan deal lowering tariffs on Japanese auto exports by mid-September.

- Japan’s broader TOPIX index edged 0.2% higher, remaining just below record highs reached earlier this week.

- China’s Shanghai Composite jumped 1.1%, while the Shanghai Shenzhen CSI 300 advanced nearly 2%.

- Chipmaking stocks rallied on renewed optimism over artificial intelligence demand after software firm Oracle secured multi-billion-dollar AI contracts, sending its shares sharply higher on Wednesday.

- Hong Kong’s Hang Seng index pared sharp losses to trade 0.3% lower, remaining close to a four-year high with sharp gains in the past few sessions.

- The Hang Seng TECH sub-index, which retreated over 1.3% in early trade, recouped all its losses to trade flat, boosted by chip stocks.

- South Korea’s KOSPI rose 0.4%, while Singapore’s Straits Times Index was largely unchanged.

- Elsewhere, Australia’s S&P/ASX 200 fell 0.5%, while India’s Nifty 50 opened largely flat.

- On the economic front, data on Wednesday showed an unexpected easing in U.S. producer price inflation for August, strengthening the case for the Fed to cut rates by a quarter-point at its September 17 meeting.

- The more widely-watched U.S. consumer prices data is due later on Thursday, and is expected to provide further clarity on how far and how fast the Federal Reserve might ease monetary policy.

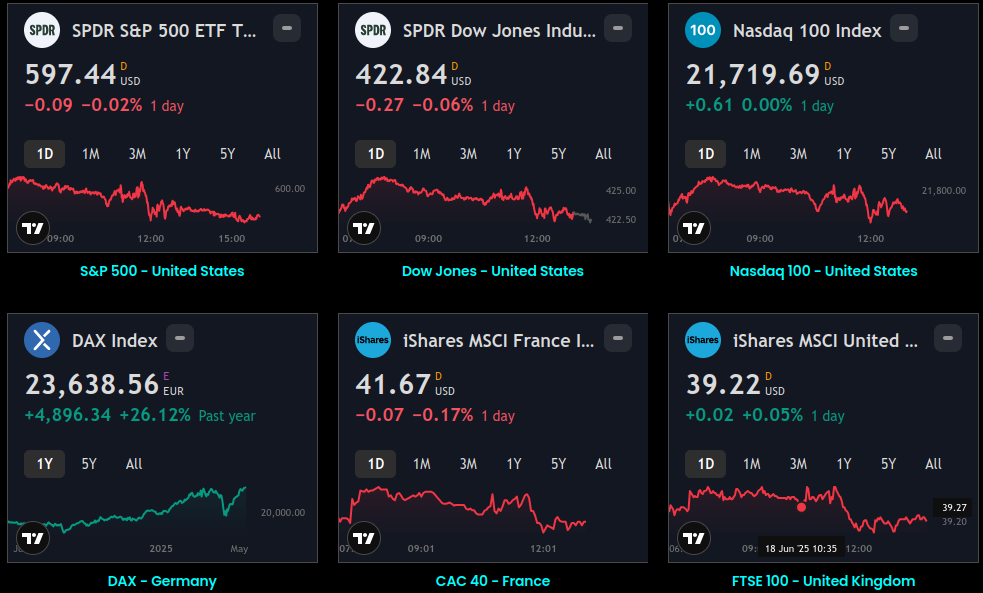

Market Close

- Equity markets finished higher on Thursday, with the S&P 500 and Nasdaq hitting record closing highs, as CPI rose to 2.9% annualized, as expected. Materials and health care stocks led to the upside, while energy was the only sector broadly lower.

- Bond yields fell, with the 10-year U.S. Treasury yield at 4.02%, likely reflecting expectations of Fed easing. In international markets, Asia was mixed, as Japan's Nikkei index and South Korea's Kospi index notched record highs. Europe finished higher, as the European Central Bank held its key deposit facility interest rate steady at 2.0%, as expected.

- The U.S. dollar declined against major international currencies. In commodity markets, WTI oil traded lower on an International Energy Agency report forecasting more OPEC+ output hikes this year.

- Consumer price index (CPI) inflation increased to 2.9% annualized in August, as expected, from 2.7% the prior month. Energy prices edged up 0.7% month-over-month, led by a 1.9% gain in gasoline, providing key drivers to the uptick of headline inflation. Core CPI, which excludes more-volatile food and energy prices, met forecasts to hold steady at 3.1%. We expect tariffs to put some additional pressure on inflation, as higher import costs are at least partially passed along to consumers.

- Initial jobless claims rose to 263,000 this past week, the highest reading in four years and well above forecasts for a pullback to 231,000. Continuing claims, which measures the total number of people receiving benefits, held steady at 1.94 million. The unemployment rate remains relatively low at 4.3%, and 7.2 million job openings are modestly below unemployment of 7.3 million.

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.

:max_bytes(150000):strip_icc()/GettyImages-22253320971-da13e4ba2de647db99b7a164cd72465b.jpg)