WTF Dailies September 04, 2025

US stock futures traded flat after the release of new data amped up anticipation for Friday's jobs report and boosted bets on a Federal Reserve rate cut this month.

- US stock futures traded flat after the release of new data amped up anticipation for Friday's jobs report and boosted bets on a Federal Reserve rate cut this month.

- On Wednesday, stocks mostly rose after the latest update on jobs openings indicated continued softening in the labor market. The data left investors feeling even more confident Fed officials will cut rates at their September meeting.

- Most Asian stocks rose on Thursday, tracking overnight gains on Wall Street amid growing optimism that the Federal Reserve will cut interest rates later in September.

- Chinese markets lagged, with local stock benchmarks tumbling from recent peaks after Bloomberg reported the country’s financial regulators were considering some curbs on stock market speculation.

- Regional markets took some positive cues from a strong overnight close on Wall Street on gains in Alphabet Inc (NASDAQ:GOOGL) and Apple Inc (NASDAQ:AAPL). Markets were also encouraged by several Federal Reserve officials flagging the potential for rate cuts due to a cooling labor market.

- Soft JOLTS job openings data released on Wednesday furthered this notion, with focus now on upcoming nonfarm payrolls data. S&P 500 Futures rose 0.1% in Asian trade, with markets on edge before the reading.

- Japan’s Nikkei 225 index was the best performer in Asia, rising 1.4%, while the TOPIX added 0.9%. Japanese markets were due for some recovery after logging a muted start to September.

- Broader Asian markets followed a similar trend. South Korea’s KOSPI rose 0.6%, extending gains after positive gross domestic product data from earlier in the week.

- Australia’s ASX 200 surged 0.9%, rebounding from steep losses in the prior session, as positive GDP data dampened some optimism over more interest rate cuts by the Reserve Bank.

- Singapore’s Straits Times index rose 0.3%, while India’s Nifty 50 index rose 0.8% in morning trade.

- Indian shares were battered by the U.S. hiking trade tariffs on the country to 50% in late-August. But comments from some Indian ministers, that trade talks were still ongoing with Washington, offered local markets relief this week.

- Softer-than-expected purchasing managers index data for August, however, dampened sentiment towards Indian markets, as local industries grappled with 25% tariffs imposed by the U.S. earlier in August.

- Regional markets tracked overnight gains in Wall Street, as several Fed officials said the central bank was considering lower rates to offset weakness in the labor market. This comes after Fed Chair Jerome Powell in August raised a similar point, although he still flagged caution over sticky inflation.

- Fed fund futures showed markets pricing in a nearly 97% chance the Fed will lower rates by 25 basis points during its September 17-18 meeting, according to CME Fedwatch.

- China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes fell 2.5% and 2%, respectively, while Hong Kong’s Hang Seng index shed 1.3%.

- Bloomberg reported that China’s financial regulators were considering some measures to cool local stock markets, amid concerns over the speed of a $1.2 trillion rally since early-August.

- Proposed measures include the removal of some short-selling curbs and more controls on speculative trading, the report said, with the measures aimed at eliciting more stability in local equity markets.

- Concerns over more government controls sparked steep losses in Chinese indexes, with markets also vulnerable to profit-taking after a strong rally in August. Chinese stocks had vastly outperformed their Asian and global peers in the prior month amid increasing optimism over local artificial intelligence efforts and stimulus measures from Beijing.

Market Close

- Equity markets finished higher on Thursday, with the S&P 500 reaching a record closing high, as investors likely await the August jobs report to be released tomorrow.

- Consumer discretionary and communication stocks led gains, while the utilities were the only sector broadly lower for the day.

- Bond yields fell, with the 10-year U.S. Treasury yield at 4.16%, potentially reflecting some investor caution ahead of tomorrow's jobs report.

- European markets rose as European Union retail sales contracted by 0.5% in July, beating forecasts for a larger 0.9% drop.

- The U.S. dollar strengthened against major international currencies.

- In commodity markets, WTI oil traded lower ahead of a meeting of OPEC countries this weekend in which producers are expected to discuss additional output hikes.

- The ADP employment survey showed that private-sector employment (excluding government workers) grew by 54,000 in August, below estimates for 85,000. The Leisure and Hospitality sector contributed nearly all of the gains, adding 50,000 jobs. Employment contraction in trade/transportation/utilities (-17,000) and education/health (-12,000) roughly offset hiring in other industries.

- The U.S. Bureau of Labor Statistics' employment report for August, known as nonfarm payrolls, to be released tomorrow, should provide additional insight, in our view, as this report includes government workers. Consensus estimates call for 80,000 jobs added, which would mark the fourth straight month of sub-100,000 employment growth, while unemployment is expected to remain unchanged at 4.2%. A soft report could help reinforce rate-cut expectations at the Fed’s September meeting.

- Initial jobless claims rose to 237,000 this past week, slightly above estimates pointing to 231,000. Continuing claims, which measures the total number of people receiving benefits, held steady at 1.94 million. The unemployment rate remains low at 4.2%, and job openings roughly equal unemployment at about 7.2 million each.

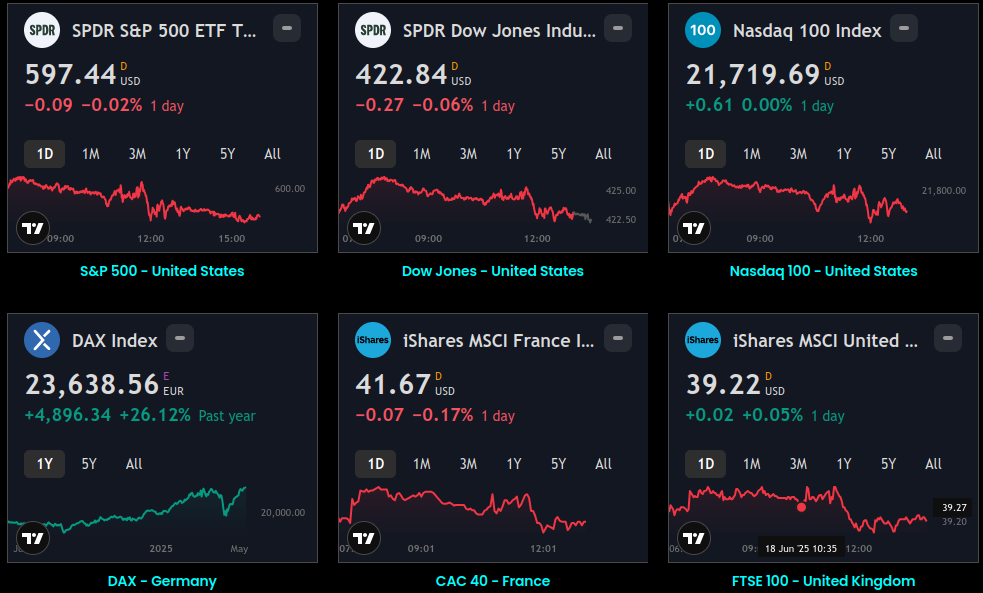

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.

:max_bytes(150000):strip_icc()/GettyImages-22253320971-da13e4ba2de647db99b7a164cd72465b.jpg)