WTF Dailies September 02, 2025

US stocks futures wavered around the flatline Monday with Wall Street set for a delayed open to the week after Monday's closure for the Labor Day holiday. Investors are braced for a tumultuous month, with legal drama around President Trump's tariffs and concerns over Fed independence in high focus.

- US stocks futures wavered around the flatline Monday with Wall Street set for a delayed open to the week after Monday's closure for the Labor Day holiday. Investors are braced for a tumultuous month, with legal drama around President Trump's tariffs and concerns over Fed independence in high focus.

- Asian stocks were a mixed bag on Tuesday as uncertainty over U.S. trade tariffs and interest rate cuts kept investors to the sidelines, while Chinese markets fell from recent peaks following mixed data for August.

- Regional markets saw a dearth of immediate trading cues following a U.S. market holiday on Monday. But S&P 500 Futures fell 0.1% in Asian trade as a legal challenge to President Donald Trump’s trade tariffs and uncertainty over an upcoming Federal Reserve meeting kept sentiment largely risk-averse.

- Focus is also on key U.S. nonfarm payrolls data due later this week, which is likely to factor into expectations for rate cuts. Markets were seen remaining largely geared towards a September cut, despite sticky inflation data released last week.

- The prospect of lower U.S. interest rates had supported Asian stocks through August, and offered some support in recent sessions.

- Japan’s Nikkei 225 rose 0.5%, while the TOPIX index added 0.7%.

- South Korea’s KOSPI was the best performer in Asia, rising 0.9% after consumer price index inflation data read softer than expected for August, opening the door for more rate cuts by the Bank of Korea.

- Singapore’s Straits Times index rose 0.4%, while Australian shares retreated on weak data.

- China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes fell 0.9% and 0.8%, respectively. Both indexes traded below multi-year highs hit last week, and also appeared to be due for some consolidation after a stellar performance through August.

- Hong Kong’s Hang Seng index fell 0.7%.

- Weak purchasing managers index readings for August, released over the past two days, dampened optimism towards Chinese markets, keeping them rangebound since Monday.

- Government PMI data showed a bigger-than-expected decline in manufacturing activity, while private PMI data showed the manufacturing sector unexpectedly grew in August, albeit at a sluggish pace.

- The readings highlighted some falling off in Chinese business activity as support from Beijing ran dry, which could in turn herald more weakness in the world’s second-largest economy. But sustained economic weakness is expected to attract even more stimulus measures from Beijing.

- Hong Kong and Chinese chipmaking stocks were the worst performers on Tuesday, as they faced some profit-taking after bets on more Chinese self reliance for artificial intelligence boosted the sector in August.

- Australia’s ASX 200 fell 0.3% on Tuesday, weighed by softer-than-expected net exports contribution data for the second quarter.

- The data showed Australia’s key commodity exports contributed far less to Q2 gross domestic product than expected. The GDP data will be released on Wednesday, and could now come in softer than expected. Market consensus is for a 0.5% quarter-on-quarter increase.

- Still, Australia logged a smaller-than-expected current account deficit in the second quarter.

- India’s Nifty 50 index opened 0.2% higher on Tuesday, but was nursing steep losses since late-August as Trump’s 50% trade tariffs against the country took effect.

- While some of these losses were offset by strong economic data from India, sentiment towards local markets remained largely negative. The rupee steadied after hitting a record low against the dollar on Monday.

- Trump on Monday claimed that India had offered to lower all tariffs on U.S. goods to zero, even as Prime Minister Narendra Modi was seen meeting Chinese and Russian leaders last week, somewhat defying pressure from Washington.

- Trade talks between Washington and New Delhi were seen largely falling through as Trump’s tariffs took effect last week. The tariffs are aimed at curbing India’s purchases of Russian oil, with U.S. officials claiming that New Delhi had funded Russia’s war with Ukraine.

- But India has so far largely rejected calls to curb Russian oil imports, given that the country is heavily dependent on foreign oil.

Market Close

- Equity markets closed lower on Tuesday following last week's U.S. court ruling against most tariffs imposed this year.

- Energy and consumer staples were among the few sectors posting gains, while real estate and industrial stocks led declines.

- Bond yields rose, with the 10-year U.S. Treasury yield at 4.27%.

- In international markets, Asia finished mixed following the Shanghai Cooperative Organization summit over the weekend that included leaders of several Asian countries, including China, India and Russia.

- Europe was down on higher bond yields, driven in part by fiscal concerns. Preliminary European Union harmonized CPI for August also ticked up to 2.1% year-over-year, slightly above forecasts to hold steady at 2.0%.

- The U.S. dollar strengthened against major international currencies. In commodity markets, WTI oil traded higher, likely reflecting concerns over potential Russian supply disruptions due to escalating Ukrainian drone strikes.

- The final S&P U.S. Manufacturing Purchasing Managers Index (PMI) for August rose to 53.0, from 49.8 the prior month, rebounding above the key 50.0 mark signaling expansion. Higher production and new orders were key drivers of output growth, though tariffs were again linked to rising input costs.

- Companies added to inventories of finished goods due in part to concerns over future prices and supply constraints.

- The Institute for Supply Management (ISM) Manufacturing PMI for August improved to 48.7, but remained in contraction territory and missed the forecast for a larger rise to 49.2. Within ISM's components, new orders and supplier deliveries were the largest positive contributors, while employment and production were the main detractors.

- The U.S. Court of Appeals for the Federal Circuit ruled that most tariffs imposed earlier this year exceed presidential authority in the International Emergency Economic Powers Act of 1977. Implementation of the decision is delayed until October to allow the administration to appeal to the U.S. Supreme Court. Tariffs on foreign steel, aluminum and autos were levied under separate trade acts and, thus, are not affected by this ruling.

- While this development introduces some additional tariff uncertainty, the Trump administration has appealed to the U.S. Supreme Court and requested an expedited ruling. The administration could also levy tariffs under alternative legal authorities, such as section 232 of the Trade Expansion Act of 1962 or the Trade Act of 1974. However, other acts generally require investigations to be conducted by the Executive branch departments, taking time to complete, and tariff rates and terms may be limited in some cases.

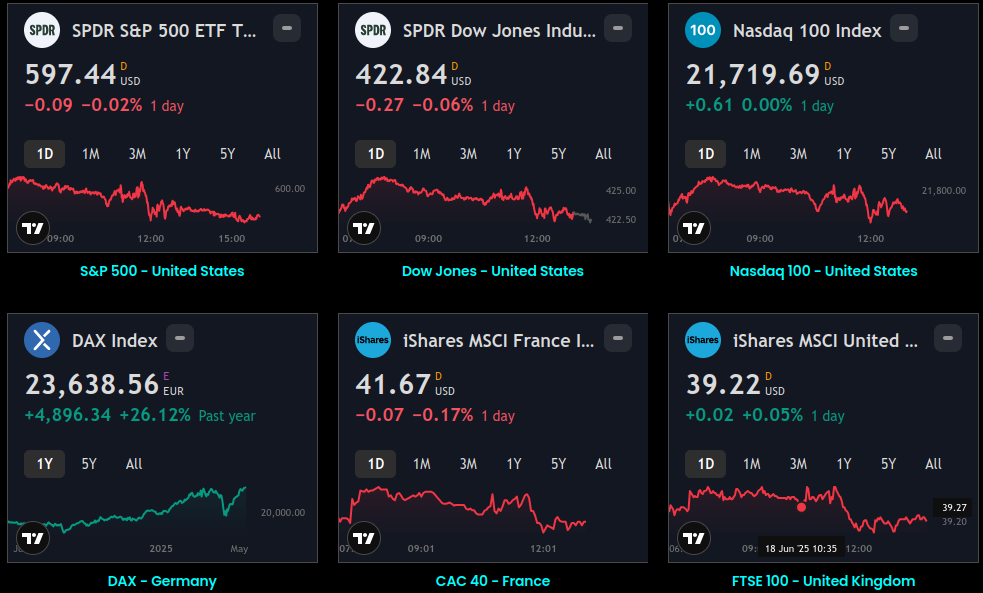

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.