WTF Dailies October 14, 2025

US stock futures flat as investors looked forward to the start of earnings season, following a strong rebound session that helped the major averages recover from Friday's tariff-driven drop.

- US stock futures flat as investors looked forward to the start of earnings season, following a strong rebound session that helped the major averages recover from Friday's tariff-driven drop.

- Earnings season kicks off Tuesday morning with JPMorgan Chase (JPM), Citigroup (C), Goldman Sachs (GS), and Wells Fargo (WFC) reporting results. The stocks of Wall Street's banks have rallied for most of the year, and analysts expect to see rising profits from the group.

- Meanwhile, with key economic reports stalled by the government shutdown, investors and the Federal Reserve lack a clear view of the economy's direction. The publication of the consumer inflation report, originally expected Wednesday, has been delayed to Oct. 24. Data on retail sales and producer prices are also expected to be pushed back.

- The blackout of economic reports puts added weight on Fed Chair Jerome Powell’s upcoming speech on Tuesday, where he is set to talk at the National Association for Business Economics (NABE) annual meeting.

- Most Asian stocks reversed some early gains to turn sharply lower on Tuesday, with markets fretting about renewed trade tensions between the U.S. and China, while Japanese shares slumped amid political uncertainty.

- Overnight, Wall Street’s major indexes posted strong gains after President Donald Trump struck a softer tone about China. However, much of Asia held back from following suit.

- U.S. stock index futures also reversed course to turn modestly lower after edging higher in early Asian hours.

- U.S. President Donald Trump last week threatened to impose 100% tariffs on Chinese imports in response to Beijing’s recent curbs on critical mineral exports, reigniting concerns of another round of tariff escalations between the world’s two largest economies.

- In an interview with Fox Business Network, Treasury Secretary Scott Bessent said Trump and Chinese President Xi Jinping were still expected to meet, offering some hope of dialogue.

- China’s Ministry of Commerce on Tuesday confirmed that working-level discussions with the U.S. are ongoing this week, while vowing to “fight till the end” against U.S. measures.

- The rhetoric prompted investors to pare back risk despite sharp gains on Wall Street overnight.

- Hong Kong’s Hang Seng index dropped 0.8% on Tuesday, extending sharp losses.

- Mainland Chinese markets edged lower after rising in early trading. The blue-chip Shanghai Shenzhen CSI 300 fell 0.4% and Shanghai Composite ticked lower.

- South Korea’s KOSPI fell 0.6% to 3,563.19 points, after jumping as much as 1.3% to 3,646.77, its highest level ever.

- Early gains were boosted by Samsung Electronics’ (KS:005930) upbeat third-quarter profit forecast. Samsung shares declined 3% after jumping nearly the same in early trade.

- Japan’s Nikkei 225 plunged 3% on Tuesday after returning from a market holiday. The move comes after Sanae Takaichi’s bid to become Japan’s prime minister faced a setback last week as her coalition partner withdrew.

- Australian S&P/ASX 200 traded flat after Reserve Bank of Australia minutes showed policymakers remained concerned about inflation pressures and offered little new guidance on the near-term policy path.

- Elsewhere, Singapore’s Straits Times Index ticked 0.3% lower. The country’s central bank left monetary policy unchanged on Tuesday, as expected.

- Preliminary data showed Singapore’s economy grew more than expected in the third quarter, but the year-on-year growth moderated compared to last quarter, as manufacturing output stagnated.

- India’s Nifty 50 were largely unchanged. Shares of LG Electronics India Ltd (NSE:LGEL) soared over 50% in their market debut on Tuesday, after its $1.3 billion initial public offering drew overwhelming investor demand.

Market Close

- Equity markets finished lower in a volatile trading session on Tuesday as trade tensions continued. China put new sanctions on U.S. units of South Korean shipbuilder Hanwha Ocean, prohibiting them from doing business in China. These actions follow the U.S. move to hike fees on Chinese ships docking at U.S. ports.

- U.S. Treasury Secretary Scott Bessent commented that President Trump still intends to meet with China's President Xi Jinping at the Asia-Pacific Economic Cooperation summit later this month.

- The U.S. government shutdown continues, reaching two weeks today, the fifth-longest in history. With the U.S. House of Representatives on recess, there does not appear to be a clear path to resolution in the near term.

- Technology and consumer discretionary stocks pulled broader indexes lower, as sector performance was mostly higher, with the consumer staples and industrial sectors leading gains.

- In international markets, Asia finished lower overnight, likely reflecting continued investor caution over trade developments.

- The U.S. dollar declined against major international currencies.

- In commodity markets, WTI oil fell near five-month lows as the International Energy Agency raised its supply forecast and cut its demand outlook.

- JP Morgan, Wells Fargo, Citigroup and Goldman Sachs released third-quarter results this morning that were ahead of estimates for both earnings and revenue. Bank of America and Morgan Stanley will follow tomorrow.

- Earnings of S&P 500 companies are forecast to rise about 8% year-over-year. Earnings growth is expected to be broad, with seven of the 11 sectors forecast to report higher earnings per share. Wider earnings growth should help drive more balanced market performance across sectors, strengthening the case for portfolio diversification. Estimates point to technology companies leading earnings growth, followed by the utility and materials sectors.

- Bond yields fell, with the 10-year Treasury yield at 4.03%. Bond markets reflect expectations for the Fed to continue its easing cycle it resumed last month to support the softening labor market. Futures markets are pricing in two more interest-rate cuts this year, followed by another two cuts or three next year, which would bring the fed funds rate down near 3.0%.

- The Fed's own projection suggests a slower pace of easing. Given the potential for economic momentum to slow, driven in part by the ongoing government shutdown, the Fed likely remains on track for one or two more rate cuts this year, followed by another one or two cuts next year. We expect lower interest rates to reduce borrowing costs for consumers and businesses, which should help provide stimulus to the economy.

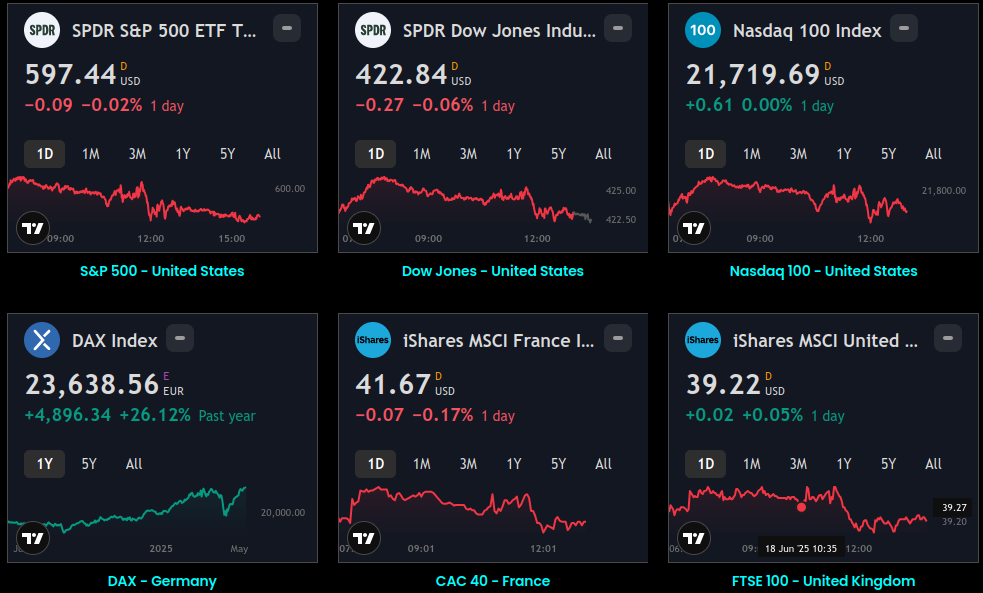

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.