WTF Dailies October 10, 2025

US stock futures rose late Thursday after the S&P 500 and Nasdaq Composite both slipped from record highs in the day session, weighed down by ongoing political gridlock in Washington.

- US stock futures rose late Thursday after the S&P 500 and Nasdaq Composite both slipped from record highs in the day session, weighed down by ongoing political gridlock in Washington.

- The government shutdown entered its ninth day Thursday, with lawmakers still unable to agree on a funding bill. The Senate failed for a seventh time to advance stopgap measures. However, change may be coming as some Republican lawmakers signaled willingness to negotiate on the healthcare subsidies Democrats insist on saving as a condition of reopening the government.

- Looking ahead, the University of Michigan's consumer sentiment reading is due Friday morning at 10 a.m. ET. In lieu of the release of government economic data during the shutdown, the report will grab investors' attention.

- Additionally, according to Bloomberg, the Bureau of Labour Statistics plans to release September's CPI by the month's end. The report will be a reprieve from the data void and provide critical insight into expectations for Federal Reserve rate cuts this year.

- Next week, investors are bracing for the start of third-quarter earnings season, with major banks including JPMorgan (JPM) and Citigroup (C) set to report their results. Earnings are expected to be softer, with analysts betting tariffs will bite into revenue for the quarter.

- Most Asian stocks fell on Friday, pressured by some profit-taking in the technology sector, while South Korean markets soared to record highs as trade resumed after a week-long break.

- Regional markets tracked overnight declines in Wall Street, which fell from record highs as a long-running tech rally paused for breath. Markets were also left wanting more cues on the U.S. economy, as an ongoing government shutdown delayed the release of several data points.

- S&P 500 Futures rose 0.2% in Asian trade, as persistent bets on an October interest rate cut by the Federal Reserve still underpinned risk appetite. A ceasefire between Israel and Hamas also kept sentiment upbeat.

- Japan’s Nikkei 225 fell 1%, while the broader TOPIX index slid 1.7%, with both indexes falling from recent record highs. Losses in tech stocks pressured the Nikkei, with tech conglomerate SoftBank Group Corp. (TYO:9984) falling 3.4% from record highs.

- Local markets were spooked by a stronger-than-expected producer price index inflation reading for September, given that sticky inflation is likely to elicit more rate hikes by the Bank of Japan.

- But the BOJ is expected to face growing resistance from the Japanese government over its rate hike plans, especially with fiscal dove Sanae Takaichi set to become prime minister.

- Japanese markets rallied this week on Takaichi’s election as the leader of the ruling Liberal Democratic Party, with a parliamentary session on her prime ministership set to convene in mid-October.

- China’s Shanghai Shenzhen CSI 300 and Shanghai Composite indexes fell 0.5% and 0.2%, respectively, pulling back from a sharp bounce in the prior session. Mainland markets resumed trade on strong footing after the golden week holiday, with government data pointing to steady consumer spending during the break.

- Hong Kong stocks lagged, with the Hang Seng index falling as much as 1%. Tech shares were the biggest weight on the index, as they fell tracking their U.S. peers.

- Semiconductor Manufacturing International Corp (HK:0981), China’s biggest chipmaker, sank 5.2% and was the worst performer on the Hang Seng.

- Losses in high-flying biotech stocks also weighed, after U.S. lawmakers pushed forward a defense bill that will bar certain Chinese biotech firms from receiving federal funding, and will also restrict American investments in sensitive Chinese industries.

- WuXi AppTec Co Ltd (HK:2359) and WuXi Biologics (HK:2269), which are targeted by the measure, fell between 2% and 3% in Hong Kong trade.

- Broader Asian markets mostly trended lower, with Singapore’s Straits Times index down 0.2%, while Australia’s ASX 200 moved in a flat-to-low range.

- Futures for India’s Nifty 50 index rose 0.2%, with a string of key tech earnings due in the coming weeks.

- South Korean markets were an outlier, with the KOSPI rallying about 1.5% to a record high of 3,617.86 points.

- Local markets rose largely in catch-up trade after a week-long holiday, with tech shares– especially chipmakers– leading the advance.

- The KOSPI surged to a record high last week after heavyweight chipmakers SK Hynix Inc (KS:000660) and Samsung Electronics Co Ltd (KS:005930) signed deals to supply memory processors to OpenAI, which represent a major revenue source for the coming years.

- Samsung and SK Hynix surged 5.1% and 6.6%, respectively, on Friday. SK Hynix hit a record high, while Samsung was at a near six-year peak.

Market Close

- Equity markets closed sharply lower on Friday, reversing gains from earlier in the week, following comments from President Trump that the U.S. may hike tariffs on imports from China. The comments came in response to China's new export controls on rare-earth minerals, which are important inputs to certain industrial applications, including semiconductors, defense and battery technology.

- Sector performance was mostly lower, with technology and consumer discretionary stocks leading declines, likely reflecting some profit-taking following strong market performance in recent months, while consumer staples was the only sector broadly higher.

- Bond yields fell, with the 10-year U.S. Treasury yield at 4.06%. In international markets, Asia and Europe also finished lower.

- The U.S. dollar declined against major international currencies.

- In commodity markets, WTI oil traded near five-month lows as the ceasefire in Gaza took effect, potentially reducing supply risks, while rising trade tensions could slow global growth.

- The focus for investors will likely turn to corporate earnings next week, with earnings of S&P 500 companies forecast to rise about 8% year-over-year. Earnings growth is expected to be broad, with seven of the 11 sectors forecast to report higher earnings per share. Wider earnings growth should drive more balanced market performance across sectors, strengthening the case for portfolio diversification, in our view.

- Estimates point to technology companies leading earnings growth, followed by the utility and materials sectors. With valuations elevated, earnings growth will likely be key to driving markets higher.

- The University of Michigan consumer sentiment index dipped to 55.0 in October, missing expectations for a rebound to 55.8 and the lowest reading in five months. Sentiment was impacted by inflation and weakening job prospects. Near-term inflation expectations edged lower to 4.6%, from 4.7% the prior month, but remained elevated.

- Long-term consumer inflation expectations held steady at 3.7%. Despite weak sentiment, consumer spending has remained resilient, providing important support to the economy.

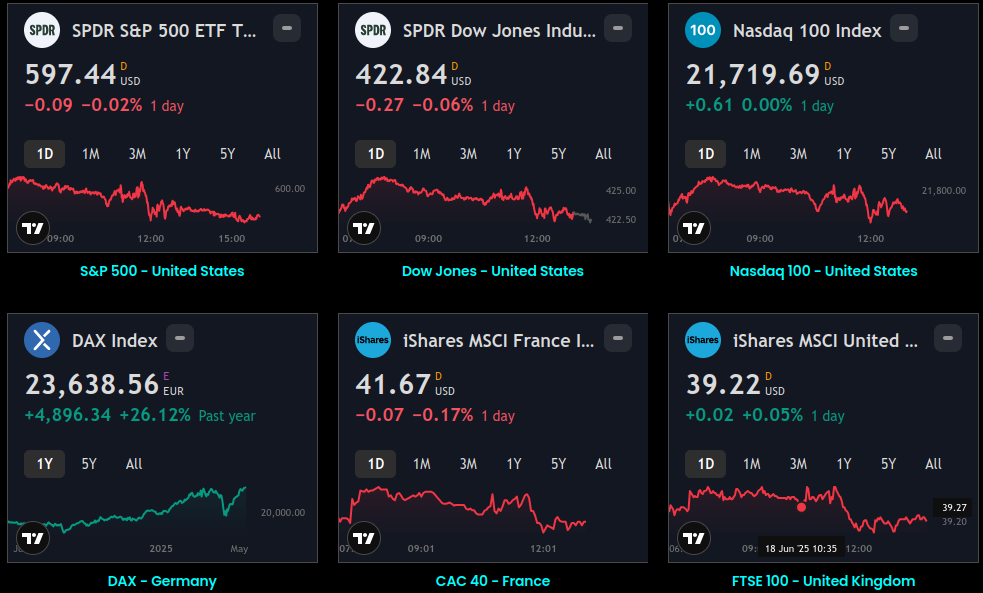

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.