WTF Dailies October 06, 2025

US stock futures rose early Monday morning as the federal government shutdown entered another week, as Wall Street looked to build on a strong run for equities that pushed major indexes to fresh record highs.

- US stock futures rose early Monday morning as the federal government shutdown entered another week, as Wall Street looked to build on a strong run for equities that pushed major indexes to fresh record highs.

- Investors have largely looked past Washington gridlock after Congress failed again to reach a funding deal, extending the government shutdown and delaying key economic releases — starting with Friday's jobs report.

- Even without fresh data, investors will get insights into the Federal Reserve’s thinking this week. Fed Governor Stephen Miran is set to speak Wednesday, followed by Chair Jerome Powell on Thursday.

- Data from non-government sources will highlight the week, with no immediate end in sight to the shutdown. The University of Michigan's consumer sentiment report for October looks likely to be the major release.

- Japanese stocks led gains across Asian markets on Monday, with the Nikkei skyrocketing to record highs after fiscal dove Sanae Takichi’s weekend election win fueled bets on more fiscal spending and stimulus from the government.

- A sharp fall in the yen also buoyed Japanese markets. Outside Japan, Asian stocks were mostly languid as market holidays in China and South Korea kept trading volumes low. Hong Kong shares fell on a pullback in technology.

- Regional markets took some positive cues from Wall Street, which clocked strong gains last week as investors largely brushed off concerns over the impact of a government shutdown.

- Focus is now on when the U.S. government shutdown will end, with a slew of U.S. economic readings having been delayed by the shutdown.

- The Nikkei 225 rallied 4.5% to a record high of 48,004.0 points on Monday, while the broader TOPIX index rose 3% to a record high of 3,232.12 points.

- Industrials were the best performers on the Nikkei, amid bets that Takaichi will push for more fiscal spending on industrialization and defense. Financials lagged on bets of slower interest rate hikes.

- Takaichi won leadership of the LDP in a run-off election held over the weekend, and is now poised to become Japan’s first female prime minister. A parliamentary session on the matter is set to convene in mid-October.

- Takaichi was viewed as the most dovish among the five front-runners for LDP leadership. She has called for more fiscal spending and tax relief to prop up what she sees as a fragile Japanese economy, and is widely expected to discourage the Bank of Japan from raising interest rates further.

- This notion was a major driver of Monday’s rally, as markets bet on more accommodative and expansionary policies under Takaichi’s prime ministership.

- The yen weakened sharply against the dollar on Monday, further benefiting the heavyweight export sector.

- Broader Asian markets kept to a tight range after logging some gains last week. Hong Kong’s Hang Seng index was the worst performer in the region, losing 0.5% on a pullback in tech shares.

- Tech was a major driver of Asian stock gains last week, amid persistent cheer over artificial intelligence-driven demand. Chipmakers were the key beneficiary of this trade, especially after OpenAI signed partnerships with major South Korean memory chip makers Samsung and SK Hynix.

- Bets on more U.S. interest rate cuts in the coming days also boosted tech.

- Among broader Asian markets, Singapore’s Straits Times index rose 0.1%, while Australia’s ASX 200 was flat.

- India’s Nifty 50 index opened 0.2% higher, coming back in sight of 25,000 points after tumbling from the levels on mounting concerns over the Indian economy, especially in the face of increased U.S. trade tariffs.

Market Close

- Stock markets were mixed on Monday, with the S&P 500 and Nasdaq moving higher, while the Dow Jones was modestly lower. The technology-heavy Nasdaq was up about 0.7%, as a deal between chipmaker AMD and OpenAI around artificial intelligence (AI) infrastructure supported the technology sector.

- Meanwhile, government bond yields inched higher on Monday, with the 10-year Treasury yield up about 0.04% to 4.16%. While yields are above their recent lows, they remain within the recent range of 4.0% to 4.5%. According to the CME FedWatch, the probability of the Federal Reserve cutting rates in October remains around 95%. In our view, given the potential for economic momentum to slow driven in part by the ongoing government shutdown, the Fed likely remains on track for one or two more rate cuts this year.

- Stock markets wrapped up the third quarter on a strong note, with the S&P 500 gaining nearly 8%. The tech-heavy Nasdaq surged 11%, and the Russell 2000, a proxy for small-cap stocks, performed even better with a 12% rally. Despite the government shutdown, investor sentiment has remained resilient, with the S&P 500 notching three additional all-time highs, bringing the year-to-date total to 31. We see two key forces that are fueling this strength. First are the secular tailwinds from AI innovation. Rapid development and adoption of AI continue to drive market leadership. Semiconductor stocks, which enable the buildout of AI infrastructure, have led gains year to date and over the past month, supported by accelerating investment in data centers and AI capabilities. And second is the cyclical momentum from lower rates. With the Fed resuming easing, rate-sensitive areas of the market are rebounding. This includes cyclical sectors such as consumer discretionary, small- and mid-cap equities, and emerging markets.

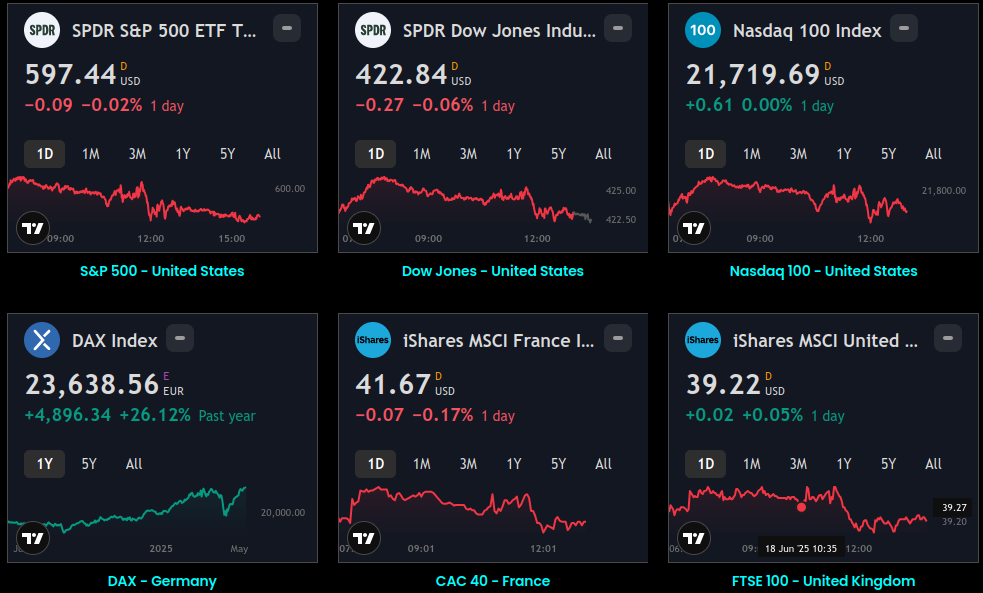

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.