WTF Dailies July 30, 2025

US stock futures traded flat as investors braced for the Federal Reserve's next interest rate decision and earnings from tech giants Microsoft (MSFT) and Meta (META).

- US stock futures traded flat as investors braced for the Federal Reserve's next interest rate decision and earnings from tech giants Microsoft (MSFT) and Meta (META).

- The Fed kicked off its two-day policy meeting Tuesday and will report its decision on interest rates Wednesday at 2 p.m. ET. With the central bank is expected to hold rates steady, Wall Street will be closely watching the Fed's "dot plot" and remarks from Fed Chair Jerome Powell for signals on potential rate cuts later this year.

- Looking forward to Thursday, Apple (AAPL) and Amazon (AMZN) will report their results. Wall Street will also get another clue as to the possible direction of interest rates with the release of the Fed's preferred inflation gauge, the Personal Consumption Expenditures (PCE) index.

- Finally, Trump's deadline for trade partners to strike deals with the US or else face blanket tariff rates looms over markets this week, with the cutoff set for Friday.

- Asian stock markets were mixed on Wednesday, with Australia gaining on a soft quarterly inflation print, though investors remained cautious ahead of key central bank decisions from the Bank of Japan and the Federal Reserve. Markets remained on edge ahead of the August 1 deadline when Washington may impose new tariffs if trade deals are not finalised.

- President Donald Trump said on Tuesday that India may face U.S. tariffs of 20% to 25%, signaling broader trade tension risks even amid progress with the European Union and China.

- Meanwhile, U.S. and Chinese officials resumed talks in Stockholm on Tuesday, aiming to extend their 90‑day tariff truce beyond its expiry on August 12.

- Sentiment remains fragile as firms and investors weigh how higher baseline tariffs and uncertainty around the August 1 U.S. deadline may curb growth and margins.

- Futures for India’s Nifty 50 edged 0.1% lower on Wednesday. In Australia, second-quarter CPI data showed inflation cooled to 2.1% year-on-year, down from 2.4%, while core trimmed‑mean inflation slowed to 2.7%.

- The surprisingly soft reading has bolstered expectations of a 25 basis point rate cut by the Reserve Bank of Australia in August.

- Australia’s S&P/ASX 200 rose 0.7% on Wednesday.

- Elsewhere, South Korea’s KOSPI jumped 0.9% on hopes of a U.S. trade deal before the deadline.

- China’s Shanghai Composite index rose 0.7%, while the Shanghai Shenzhen CSI 300 climbed 0.8%.

- Hong Kong’s Hang Seng index edged 0.3% lower after trimming some early losses. Singapore’s Straits Times Index ticked down 0.2%.

- Investors are now turning to policy actions from the Bank of Japan and the U.S. Federal Reserve.

- The BOJ is expected to hold rates steady on Thursday but may offer a brighter economic outlook following Japan’s trade deal with the U.S.

- Japan’s Nikkei 225 was largely unchanged on Wedneday, while the broader TOPIX index gained 0.4%. Fed officials began a two‑day meeting on Tuesday, with a rate decision due on Wednesday. The central bank is widely expected to keep rates at 4.25%‑4.50%.

Market Close

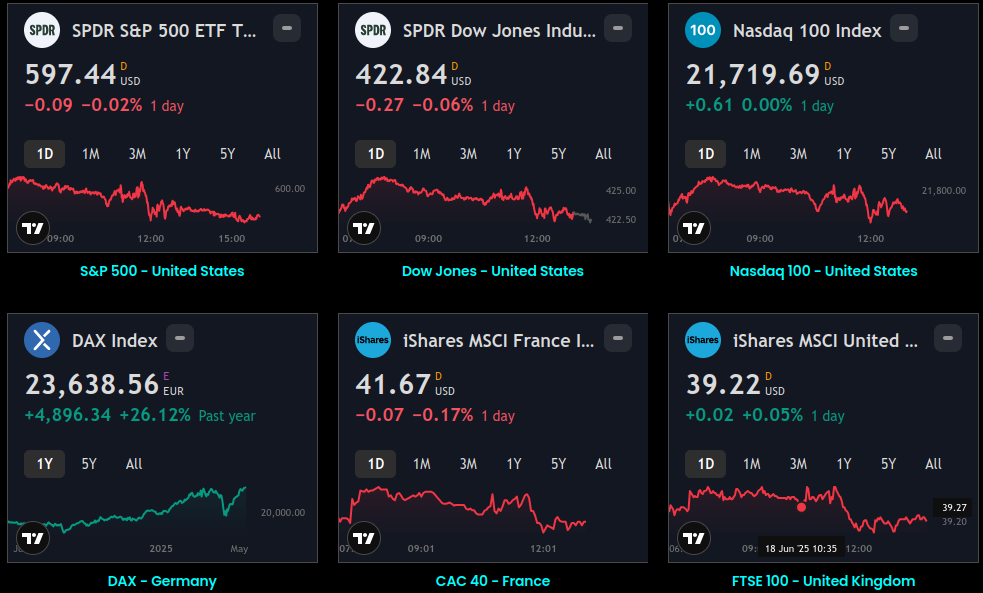

- U.S. stock markets were down modestly on Wednesday, with the technology-heavy Nasdaq outpacing the S&P 500 and Dow Jones. The Federal Reserve kept interest rates on hold at 4.25% to 4.5%, while Fed Chair Jerome Powell noted that no September interest-rate decision has been made.

- Bond yields also moved higher across the curve, as the 2-year Treasury yield, which is more impacted by the fed funds rate, moved up more, up about 0.07% to 3.94%. This comes as initial readings indicate that the U.S. economy grew modestly in the second quarter, and as the U.S. dollar rose for a fifth straight day.

- As expected, the Federal Reserve held interest rates steady at 4.25% - 4.50%. Fed Chair Jerome Powell noted that while interest rates are currently moderately restrictive, the FOMC will seek more information on the impact of tariffs in the months ahead. Powell outlined that the Fed's base-case scenario is that tariffs will pose a one-time price increase, and inflation should moderate beyond that. If we do see inflation data come in no worse than expected or jobs data deteriorate in the coming months, a September cut is possible, with Powell potentially alluding to this at the Fed's annual Jackson Hole meeting on August 21-23. We expect one to two cuts in the second half of 2025, followed by additional easing in 2026 as the Fed moves slowly toward a neutral rate (around 3%-3.5%).

- The preliminary estimate of U.S. GDP increased 3% annualized in the second quarter, registering a bounce-back from the 0.5% contraction reported in the first quarter*. This swing largely reflected an unwind in the frontrunning of imports seen early in the year, which had weighed on growth, as U.S. corporates looked to front-run potential tariffs. Excluding the large contributions from net trade and inventories, underlying domestic demand was up a more modest 1.1% annualized over the quarter, the weakest reading seen since 2022. This downshift from the 1.5% gain in the first quarter reflected softer business investment and cautious consumer spending.

- Growth is likely to remain subdued over the second half of 2025, as we see a more pronounced impact from tariffs on corporate margins and household purchasing power. However, robust balance sheets and supportive financial conditions should provide some ballast, in our view, as should potential interest-rate cuts from the Fed later this year.

Global Indices:

Active Stocks:

Stocks, ETFs and Funds Screener:

Forex:

CryptoCurrency:

Events and Earnings Calendar:

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.