WTF Dailies August 5, 2025

US stock futures pushed up as Wall Street regained its balance after a tumultuous week and braced for the next wave of corporate earnings.

- US stock futures pushed up as Wall Street regained its balance after a tumultuous week and braced for the next wave of corporate earnings.

- Palantir (PLTR) stock rose in after-hours trading after the company's earnings report beat expectations and revealed its revenue had topped $1 billion in a quarter for the first time.

- On Monday, stocks sharply rebounded after tanking on Friday in the aftermath of a number of market-shaking events, including a weak jobs report, fresh tariffs, new signs of rising prices, and the firing of the commissioner of the Bureau of Labor Statistics. President Trump continued to amp up pressure on trade Monday, threatening to hike tariffs on India.

- Wall Street is now focused on the continuation of earnings season. On Tuesday, AMD (AMD) and Rivian (RIVN) are set to report their results. McDonald's (MCD) and Disney (DIS) earnings land Wednesday. However, another trade blow looms at the end of the week, with Trump's latest iteration of global tariffs set to take effect.

- Asian stocks advanced on Tuesday, tracking Wall Street’s strong rebound after soft U.S. jobs data boosted expectations of a Federal Reserve rate cut, while investor sentiment remained cautious amid heightened global trade tensions.

- Focus also turned to the Reserve Bank of India’s ongoing policy meeting, with the central bank widely expected to keep interest rates unchanged on Wednesday.

- South Korea’s KOSPI index led gains with a 1.6% jump, while Australia’s S&P/ASX 200 also rose over 1%.

- Japan’s Nikkei 225 gained 0.6%, while the broader TOPIX index traded 0.7% higher.

- China’s Shanghai Composite index rose 0.5%, while the Shanghai Shenzhen CSI 300 edged 0.3% higher.

- Bucking the regional trend, Hong Kong’s Hang Seng index edged 0.2% lower on Tuesday.

- Elsewhere, Singapore’s Straits Times Index rose 0.5%.

- On trade policy fronts, markets continued to wrestle with renewed tariff threats from President Trump. He warned of raising tariffs on Indian imports over Russian oil purchases, adding another layer of uncertainty to markets already facing sweeping trade measures announced last week.

- Futures for India’s Nifty 50 edged up 0.2% on Tuesday.

- Meanwhile, the Reserve Bank of India’s Monetary Policy Committee convened its three-day meeting on Monday with a decision due on August 6.

- Markets expect the central bank to hold its policy rate at 5.50% after a frontloaded 0.5% cut in June. The central bank adopted a neutral stance in June, signaling future rate cuts will hinge on new economic data.

- With headline inflation slowing, the RBI has leeway to cut rates again, but robust economic growth in the first quarter and global uncertainties around tariffs could see the central bank holding rates steady. “With real rates still elevated, we continue to expect a 25 bp cut later this year in the fourth quarter,” ING analysts said in a recent note.

Markets Close

- U.S. stocks wiped out early gains to close the day lower after a weak services ISM report pointed to slowing activity and rising price pressures in this important sector. The S&P 500 fell by 0.5%, led by declines in utilities, tech and communication services, and undermining some of the rebound seen at the start of the week. Small-cap equities fared better, with the Russell 2000 index up 0.6% over the session, and now 2.2% over the week thus far, while north of the border Canadian equities rallied hard as investors played catch-up following Monday's Civic Holiday market close.

- The 10-year U.S. Treasury yield was flat over the session and continues to trade close to three-month lows following the sharp rally after Friday's weak nonfarm-payrolls report. The dollar was broadly stable against a trade-weighted basket of currencies, and oil prices fell again as the market continues to parse OPEC supply announcements and the prospect of weaker U.S. growth.

- Rising expectations for Fed interest-rate cuts helped support the rebound in equities at the start of this week, in our view. Markets had been pricing around 30 basis points (0.30%) of cuts through the rest of this year after the FOMC meeting last week, but in the wake of disappointing payrolls data this bet has doubled to around 60 basis points (0.60%), with the odds on a 25 basis points (0.25%) move in September seen at around 90%. The reaction from FOMC members to the labor report has been mixed, with Williams, Bostic and Hammack all playing down the softness in July, although a more alarmed Daly speculated that "more than two rate cuts" might be needed this year.

- Trade data this morning confirmed the tightening in the U.S. deficit reported in June, with imports down sharply, reversing the surge seen earlier this year as firms looked to front-run tariffs. This swing was visible in Canadian trade data released this morning too, which showed a rise in the trade deficit in June, in part due to weak exports to its largest trade partner south of the border. Otherwise, signs of disruptions from trade policy are starting to emerge in U.S. survey data, with the services ISM reporting the most acute price pressures in the sector since 2022 and that growth had slowed to a near standstill.

- Meanwhile, trade policy headlines continue to roll in, with President Trump indicating that an agreement to extend the trade truce with China beyond August 12 was close, and that tariffs on semiconductor and pharmaceutical imports were coming in the next week or so.

- Outside of trade, the president commented that Treasury Secretary Bessent does not want to be nominated to be the next Fed chair and that he intends to nominate a new head for the U.S. Bureau of Labor Statistics this week .

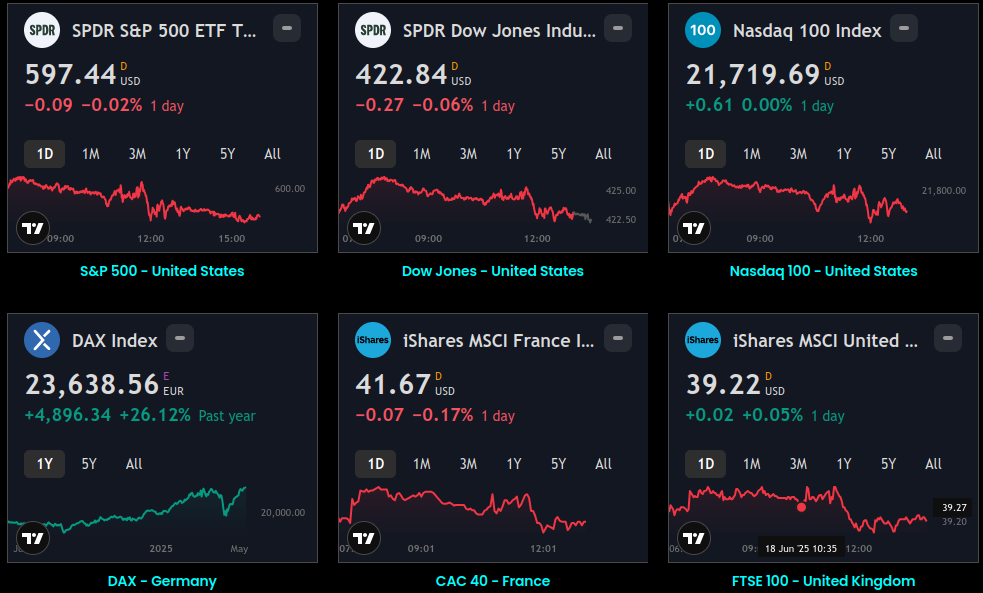

Global Indices:

Global Indices Dashboard

S&P 500 - United States Dow Jones - United States Nasdaq 100 - United States DAX - Germany CAC 40 - France FTSE 100 - United Kingdom Nikkei 225 - Japan EWH - Hong Kong Sensex - India ASX 200 - Australia MOEX - Russia MERVAL - Argentina Bovespa

Active Stocks:

Active Stocks

See the top five gaining, losing, and most active stocks for the day. It updates based on current market activity – so you’ll always see the most relevant stocks Track all markets on TradingView

Stocks, ETFs and Funds Screener:

Stocks, ETFs and Funds

Separate the wheat from the chaff – handy for sorting symbols both by fundamental and technical indicators. Sort Assets and Filter by Region, Type, Sector, Industry and Country

Forex:

Foreign Exchange Dashboard

Heatmap and Real-time quotes of selected currencies in comparison to other major currencies. Sort currencies both by fundamental and technical indicators

CryptoCurrency:

Crypto Currency Dashboard

CRYPTO HEATMAP OVERVIEW Assets by Market Capitalization

Events and Earnings Calendar:

Events & Earnings

Keep an eye on key upcoming economic events, announcements, and news. Track all markets on TradingView

This daily briefing is curated from a wide range of reputable sources including news wires, research desks, and financial data providers. The insights presented here are a synthesis of key developments across global markets, intended to inform and spark thought.

No Investment Advice: This content is for informational purposes only and does not constitute investment advice, recommendation, or endorsement.

Timing Note: Each edition is assembled based on the market context available at the time of writing. Timing, emphasis, and interpretations may vary depending on global developments and publishing windows.